1. Introduction: The Global Imperative for Indian Portfolios

For decades, the Indian retail investor has operated under the shadow of "Home Bias"—a psychological and financial inclination to anchor 100% of one’s capital within domestic borders. Historically, this was framed as a safety net; however, in a hyper-interconnected global economy, this domestic-only focus has transitioned from a security measure into a concentrated geographic risk. Modern portfolio theory dictates that true resilience is not found in proximity, but in diversification across non-correlated markets, specifically by gaining exposure to the world’s most dominant economic engine: the United States.

The strategic necessity of the US market is rooted in its role as the primary incubator for Global Innovation Leaders. Corporations such as Apple, Microsoft, Nvidia, Tesla, and Alphabet (Google) are the architects of the modern world. For the sophisticated Indian investor, these are not merely stocks; they are indispensable technological utilities with no direct equivalents on Indian bourses. Whether it is the frontier of Generative AI or the global infrastructure of cloud computing, these entities capture value that local indices cannot mirror.

The data-driven rationale for this shift is undeniable. During the market correction of late 2024 through early 2025, the Nifty 500 TRI suffered a significant drawdown of 18.1%. In contrast, investors who maintained a 25% allocation to a US-diversified portfolio (specifically the S&P 500) saw their overall portfolio decline by only 12.5%. This represents a 32% reduction in downside volatility. While the appetite for these resilient returns has always existed, the method of execution has recently undergone a radical, state-sponsored transformation via GIFT City.

2. The Legacy Landscape: How Indians Invested Previously

Before the institutionalization of GIFT City, the "offshore" investment model was a friction-heavy endeavor reserved primarily for High Net Worth Individuals (HNIs). The administrative hurdles acted as a structural gatekeeper, effectively discouraging the broader retail class.

The legal foundation for this remains the Liberalised Remittance Scheme (LRS). Established by the RBI, the LRS allows resident individuals to remit up to $250,000 per financial year for permissible capital and current account transactions. However, the traditional workflow was arduous:

1. International Brokerage Onboarding: Investors had to manually open accounts with foreign-domiciled brokers, often involving weeks of physical documentation.

2. Forex Inefficiency: Navigating bank-level currency conversion resulted in significant "leakage" due to opaque spreads on the Telegraphic Transfer (TT) rates.

3. The Form A2 Obstacle: Every remittance required manual filing of Form A2 and the payment of high international wire fees.

4. The Repatriation Burden: Under FEMA guidelines, any unspent or unused foreign exchange must be repatriated and surrendered to an Authorised Dealer within 180 days of the date of realization or purchase, unless reinvested. This created a persistent compliance clock that many retail investors found difficult to manage.

While the old system functioned, its inherent inefficiencies acted as a "compliance tax" on global ambition.

3. The Friction Points: Why the Old System Stalled

In any financial ecosystem, friction is the enemy of scale. The legacy system’s primary failure was its inability to provide a seamless, high-velocity bridge for capital.

* Cost Prohibitiveness: High conversion spreads and flat wire fees meant that small-ticket retail entries were mathematically unviable. Fixed costs often consumed the first 2-3% of the initial investment.

* Temporal Lag: The time-intensive nature of international wire settlements meant that investors often missed volatile market entry points. By the time funds were credited to a US broker, the "dip" had often already been bought.

* The Compliance Burden: The mental load of tracking FEMA compliance, managing W-8BEN filings, and ensuring proper reporting of foreign assets created a psychological barrier.

* Limited Transparency: Access was effectively "gatekept" by a lack of unified regulation, leaving investors to navigate a fragmented landscape of third-party apps and offshore entities.

4. Decoding GIFT City: India’s International Financial Frontier

Gujarat International Finance Tec-City (GIFT City) is a regulatory masterstroke. It is not merely a real estate project in Ahmedabad; it is a Special Economic Zone (SEZ) designated as India’s first International Financial Services Centre (IFSC).

The strategic "Alpha" of GIFT City lies in its unique status: it is physically located in India but legally treated as "outside India" for the purposes of foreign exchange regulations under FEMA. This allows for a unique environment where transactions occur in foreign currencies (USD, EUR, GBP) while remaining under the watchful eye of a domestic regulator.

The ecosystem is governed by the International Financial Services Centres Authority (IFSCA). The IFSCA acts as a unified, powerful regulator that consolidates powers traditionally held by SEBI, RBI, and IRDAI. This streamlined authority ensures that GIFT City operates at the speed of global markets rather than the speed of local bureaucracy.

5. The Paradigm Shift: Simplified Global Access

The structural shift from "Outward Remittance" to "Domestic-International Trading" has fundamentally democratized global markets.

NSE IX and Global Access The NSE International Exchange (NSE IX) has revolutionized access via Unsponsored Depository Receipts (UDRs). These receipts represent fractional ownership of US-listed stocks like Nvidia or Microsoft, allowing retail participants to buy shares in small denominations. Furthermore, the NSE IX Global Access platform is rapidly expanding; while it started with Wall Street, it is currently the gateway to 30 global markets, including the UK, Japan, and major European bourses.

Friction Reduction

* Digital Onboarding: Utilizing DigiLocker, Aadhar, and PAN, the KYC process for an IFSC account is often completed in under one minute.

* Foreign Currency Accounts (FCA): Investors can now maintain FCAs within GIFT City, allowing them to hold USD liquidity and trade without constant conversion fees for every transaction.

* Repatriation Ease: Since the funds stay within the Indian IFSC ecosystem, the operational risk of the 180-day repatriation rule is significantly mitigated for active traders.

6. Implementation Guide: Step-by-Step Investment

To move capital from a domestic savings account to the Nasdaq, follow this operational roadmap:

1. Account Setup: Open a trading and demat account with an IFSCA-registered broker and a linked Foreign Currency Account (FCA) with a GIFT City bank.

2. Funding via LRS: Remit INR from your domestic bank to your GIFT City FCA. This is a single LRS transaction where funds are converted to USD.

3. Execution: Access the NSE IX platform during global market hours. You can purchase UDRs of US stocks or invest in Global ETFs directly.

4. Settlement: Trades are settled digitally within the GIFT City ecosystem, providing a faster cycle than traditional international wire models.

7. The "Alpha" of the New System: Diversification and Currency Hedges

A Senior Strategist views global diversification not as a luxury, but as a wealth-building necessity. The "Double-Whammy" effect of US investing provides a unique tailwind for Indian portfolios.

Portfolio Resilience Historical simulations show that a 20-year ₹10,000 monthly SIP in a 100% Indian portfolio would have yielded ₹1.1 crore. However, a portfolio with a 25% allocation to the S&P 500 TRI would have reached ₹1.2 crore. This extra ₹10 lakh of terminal wealth is the direct result of geographic diversification.

The Currency Hedge Synthesis The Indian Rupee has depreciated against the US Dollar by an average of 3.6% annually over the last five years. When you invest in USD-denominated assets, you capture this depreciation as a gain.

* The Calculation: If the US market returns 10% in a year and the INR depreciates by 3.6%, the effective return for an Indian investor is approximately 13.6% before taxes. This currency movement acts as a "stabilizing shock absorber." When the Indian economy or the Rupee falters, your US assets appreciate in INR terms, cushioning the blow to your net worth.

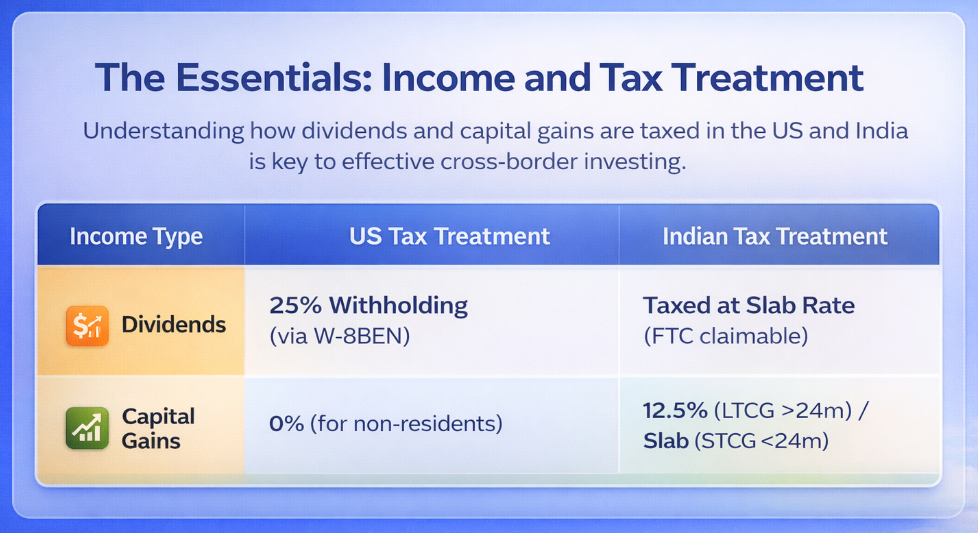

8. The Tax Architect: Navigating DTAA and Obligations

Tax efficiency is what separates gross returns from real, spendable wealth. As a strategist, you must master the India-US Double Taxation Avoidance Agreement (DTAA).

The India-US DTAA (Articles 4, 10, 13, and 24) The treaty’s legal anchor is Article 4 (Tax Residency); you must hold a valid Tax Residency Certificate (TRC)—obtained by filing Form 10FA and receiving Form 10FB—to qualify for treaty benefits. Article 24 (Limitation on Benefits) prevents treaty shopping, ensuring only genuine residents benefit.

Critique Note: The widely misquoted 15% dividend rate applies only to corporate entities with 10% ownership. Retail investors pay 25%.

TCS Provisions (Budget 2025) The Finance Act 2025 revised the Tax Collected at Source (TCS) thresholds to improve liquidity:

* Standard Investment: Nil up to ₹10 Lakhs; 20% above ₹10 Lakhs.

* Education Loans: In a major move for families, TCS on remittances for education via loans from specified financial institutions has been reduced to Nil.

Mandatory Compliance Checklist:

* Form W-8BEN: Must be filed with the broker to certify non-resident status. It expires every three years.

* Form 1042-S: You must collect this from your US broker by mid-February annually to verify the taxes withheld.

* Form 67: This must be filed on the income tax portal before the ITR deadline to claim Foreign Tax Credit (FTC).

* Exchange Rate Rule: All conversions for tax purposes must use the SBI Telegraphic Transfer (TT) Buying Rate as of the last day of the month preceding the transaction.

The Disclosure Mandate Failing to file Schedule FA (Foreign Assets) in ITR-2 or ITR-3 is a catastrophic mistake. It is mandatory even if you have zero gains. Under the Black Money Act, non-disclosure triggers a mandatory ₹10 Lakh penalty—a cost that can incinerate years of market gains.

9. Risk Management: What Investors Must Monitor

Global investing is not a risk-free endeavor. A balanced strategy requires constant vigilance:

* Market Volatility: US markets are highly sensitive to US Federal Reserve interest rate decisions and global macro shifts.

* Currency Correlation: An OLS regression analysis confirms a strong inverse relationship between the Rupee and the domestic market. For every ₹1 of Rupee depreciation, the Nifty index correlates to an approximate 149-point fall. Your US allocation serves to hedge this specific risk.

* The "Compliance Clock": Beyond the 180-day repatriation rule, you must ensure your TRC (Form 10FB) is renewed annually, as it is only valid for one financial year.

10. Conclusion: The Future of Globalized Indian Wealth

The evolution from a restrictive, friction-heavy legacy regime to the world-class financial hub of GIFT City marks a pivotal moment in Indian financial history. Global diversification is no longer an optional luxury for the elite; it is a fundamental requirement for the "Crorepati" mindset.

By democratizing access to the world’s most powerful innovation leaders—not just in the US, but across 30 global markets—GIFT City has provided the tools to build truly multi-generational, resilient wealth. The gateway to the world is no longer an offshore dream; it is a domestic reality. The strategist's move is clear: hedge your home-bias risk, capture the currency tailwind, and institutionalize your global portfolio today.